As a small business owner, I understand the constant balancing act of managing cash flow. Unexpected expenses, seasonal fluctuations, and exciting growth opportunities can all put a strain on your finances. That’s where a business line of credit can be a game-changer. In this personalized guide, I’ll share my insights on how to find the best business line of credit to support your unique needs and keep your company thriving.

Whether you’re looking to smooth out cash flow, take advantage of new opportunities, or build up your business credit, a well-chosen line of credit can provide the flexibility and financial cushion you need. But with so many lenders and options out there, the process of selecting the right one can feel daunting.

That’s why I’m here to walk you through the key factors to consider, share my strategies for comparing lenders, and provide you with the confidence to make the best decision for your business. By the end of this article, you’ll have the knowledge and tools to find the perfect business line of credit to fuel your success.

Understanding the Power of a Business Line of Credit

A business line of credit is a revolving credit account that gives you access to a predetermined amount of funds. Unlike a traditional loan where you receive a lump sum upfront, a line of credit allows you to borrow and repay funds as needed, only paying interest on the amount you’ve actually used.

This flexibility makes a business line of credit an invaluable tool for managing short-term cash flow needs, funding unexpected expenses, or capitalizing on growth opportunities. Whether you need to cover a seasonal slump, finance a new marketing campaign, or stock up on inventory, a well-timed line of credit can provide the financial cushion you need to keep your business thriving.

The key benefits of a business line of credit include:

- Cash Flow Management: Smoothing out fluctuations in your cash flow and ensuring you have the funds to cover expenses, even during slow periods.

-

Growth Opportunities: Having a line of credit as a financial safety net can make it easier to seize new opportunities, such as expanding your product line or opening a new location.

-

Building Business Credit: Making timely payments on your line of credit can help build your business credit score, leading to better financing terms in the future.

Of course, business lines of credit also come with some potential drawbacks, like variable interest rates and the risk of overspending. As an experienced business owner, I always recommend carefully weighing the pros and cons to ensure a line of credit is the right fit for your company.

Navigating the Different Types of Business Lines of Credit

When it comes to business lines of credit, there are a few key distinctions you’ll want to be aware of:

Revolving vs- Non-Revolving Lines of Credit

Revolving Lines of Credit: With a revolving line of credit, your credit limit replenishes as you repay the borrowed funds. This means you can borrow, repay, and borrow again, giving you ongoing access to the funds.

Non-Revolving Lines of Credit: Non-revolving lines of credit have a fixed credit limit that is exhausted once you’ve borrowed the full amount. If you need additional funds, you’ll have to reapply for a new line of credit.

Secured vs- Unsecured Lines of Credit

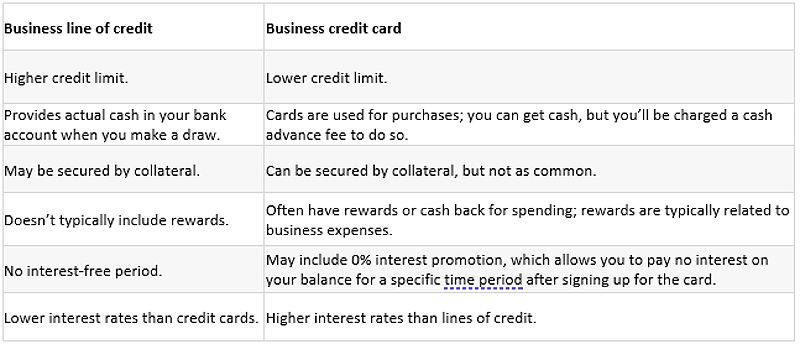

Secured Lines of Credit: Secured lines of credit require you to put up collateral, such as real estate, equipment, or inventory, to secure the financing. While this can make it easier to qualify and potentially result in lower interest rates, it also puts your assets at risk if you default on the loan.

Unsecured Lines of Credit: Unsecured lines of credit do not require collateral, but may come with higher interest rates due to the increased risk for the lender.

Depending on your business’s financial situation and needs, one type of line of credit may be better suited than another. As you evaluate your options, be sure to carefully consider the pros and cons of each to find the perfect fit.

Finding the Best Business Line of Credit for Your Needs

Now that you have a solid understanding of the different types of business lines of credit, let’s dive into the process of selecting the best one for your specific needs. Here’s my step-by-step guide to help you navigate this important decision:

-

Determine Your Financing Needs: Start by evaluating how much money you need and for what purpose. Are you looking to cover seasonal expenses, fund a new marketing campaign, or have a financial cushion for unexpected costs? Understanding your unique needs will help you narrow down your options.

-

Research and Compare Lenders: Explore a variety of lenders, including traditional banks and online/alternative providers. Compare their interest rates, fees, credit limits, and other terms to find the best fit for your business. Don’t be afraid to ask questions and negotiate to get the most favorable deal.

-

Consider Your Credit Score: Your personal and business credit scores will play a significant role in the interest rate and credit limit you qualify for. If your credit is less than perfect, you may still be able to secure a line of credit, but the terms may be less favorable. I recommend reviewing your credit report and taking steps to improve your score before applying.

-

Understand the Fees: In addition to interest charges, business lines of credit may come with other fees, such as draw fees, annual fees, or late payment penalties. Make sure you understand all the potential costs associated with the financing.

-

Read the Fine Print: Carefully review the loan agreement and terms before signing. Pay close attention to the repayment schedule, any collateral requirements, and any restrictions on how you can use the funds. It’s important to fully understand the terms and conditions before committing to a line of credit.

By taking the time to research and compare options, you’ll be better positioned to find the best business line of credit to support the unique needs of your company. Remember, it’s not just about getting approved — it’s about finding the right financing tool to help your business thrive.

Strategies for Maximizing Your Business Line of Credit

Once you’ve secured a business line of credit, it’s important to use it strategically to get the most out of this powerful financing tool. Here are a few tips to keep in mind:

-

Use it for Short-Term Needs: Avoid using a business line of credit for long-term investments or large, one-time expenses. Instead, leverage the flexibility of a line of credit to cover short-term cash flow gaps or capitalize on new opportunities.

-

Pay it Back Promptly: Make timely payments on any funds you borrow to avoid accruing high-interest charges and maintain a good business credit score. This will also help you maintain a strong relationship with your lender.

-

Monitor Your Credit Limit: Keep a close eye on your borrowing activity and ensure you don’t exceed your credit limit, which could result in penalties or a reduction in your available funds.

-

Use it as a Safety Net: Consider your business line of credit as a financial safety net, to be tapped into only when necessary. Having this resource available can provide peace of mind and help you weather unexpected challenges.

By using your business line of credit wisely and in alignment with your company’s needs, you can unlock the true power of this flexible financing tool and take your business to new heights.

FAQ

Q: What is the average interest rate for a business line of credit?

A: Interest rates for business lines of credit can vary widely, ranging from 5% to 20% or higher, depending on factors such as your credit score, time in business, and the lender.

Q: Can I get a business line of credit with bad credit?

A: While it may be more challenging to secure a line of credit with bad credit, some lenders specialize in working with businesses that have less-than-perfect credit. You may be offered higher interest rates and lower credit limits, and you may need to provide collateral.

Q: How long does it take to get approved for a business line of credit?

A: The approval process can vary depending on the lender, but some online lenders can approve applications within 24 hours or less. Traditional lenders may take longer, sometimes weeks or even months.

Conclusion

In today’s dynamic business landscape, a well-chosen business line of credit can be the key to unlocking your company’s full potential. By understanding the different types of lines of credit, evaluating your specific needs, and comparing lender options, you can find the perfect financing tool to support your growth and success.

Remember, the best business line of credit is the one that aligns with your unique goals and cash flow requirements. Take the time to do your research, crunch the numbers, and make an informed decision. With the right line of credit in your arsenal, you’ll be well on your way to navigating any financial challenges and seizing new opportunities with confidence.

If you need any further guidance or have additional questions, don’t hesitate to reach out. I’m here to support you every step of the way as you embark on this exciting journey of finding the best business line of credit for your business.